Decentralized monetary systems and central banks represent two very different approaches to managing money. Central banks, like the Federal Reserve, control monetary policy, stabilize economies, and build trust through central authority. In contrast, decentralized systems like Bitcoin operate without a central authority, offering financial autonomy but relying on distributed networks for governance and security.

The key differences come down to a few core trade-offs. Central banks manage money supply, control inflation, and provide stability, but they centralize power in ways that can limit individual financial freedom. Decentralized systems offer autonomy and transparency through blockchain technology but face challenges around scalability, security, and regulatory uncertainty. Centralized systems process transactions faster due to established infrastructure; decentralized ones are often slower but operate around the clock. Central banks act as lenders of last resort during crises, while decentralized systems rely on algorithms that can be less reliable under stress. Looking ahead, the future likely involves a mix of both, leveraging the strengths of each to create a more inclusive and efficient financial ecosystem.

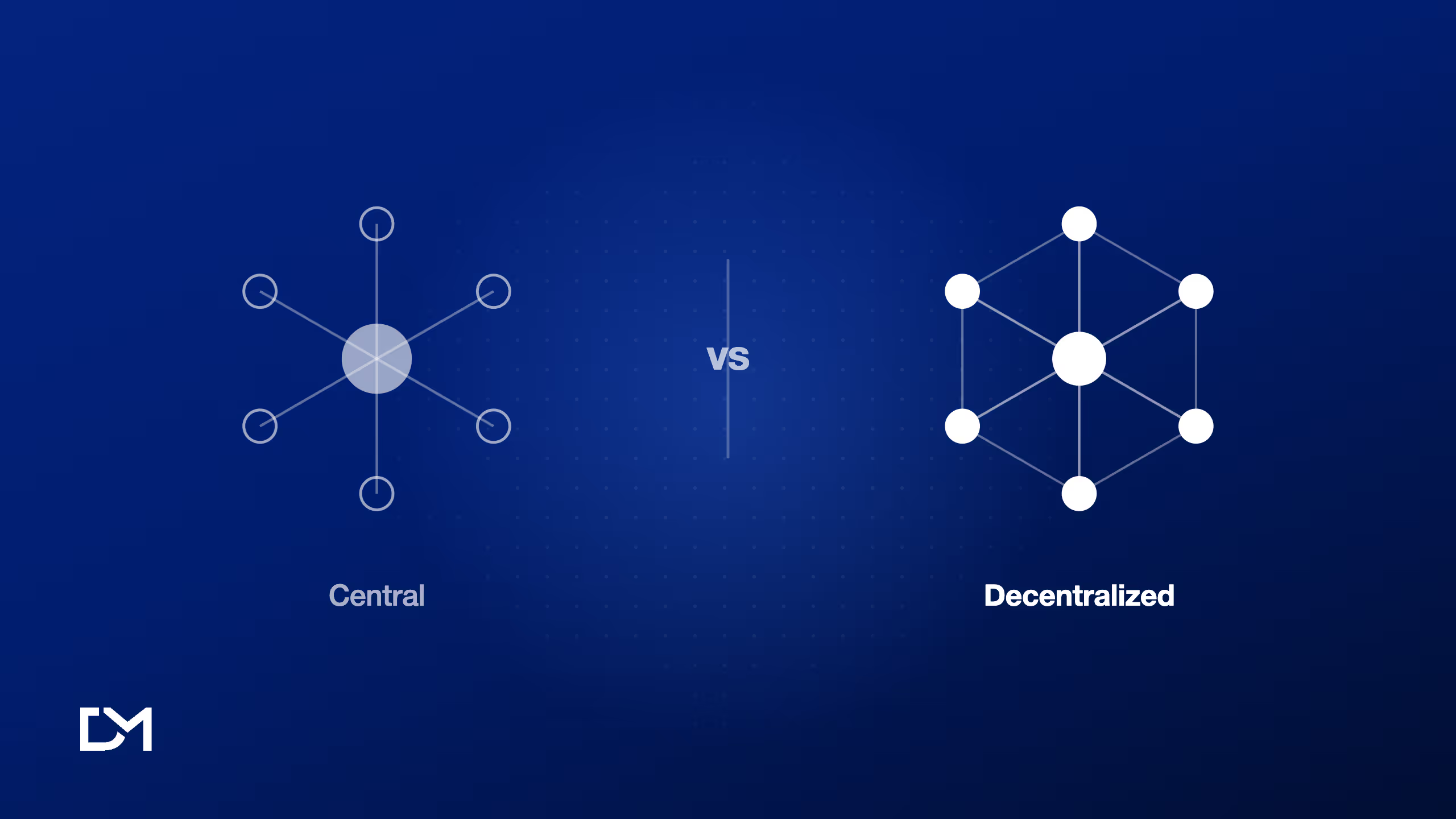

Control and Governance

The way financial systems are governed plays a major role in shaping interest rates and cross-border transactions. Central banks, such as the Federal Reserve, operate through a top-down structure where monetary authority is concentrated in the hands of appointed officials. The Fed's Board of Governors, comprising seven members appointed by the President and confirmed by the Senate, makes critical decisions including open market operations, interest rate setting, and the deployment of tools to maintain economic stability.

Central banks face inherent limitations. Fixed exchange rate systems restrict their ability to implement independent monetary policies, and the Fed's actions have far-reaching global consequences, since U.S. monetary policy directly impacts international markets and currency values. Organizations like the IMF support central bank authority by offering policy guidance and technical assistance, while transparency codes help sustain public trust.

Decentralized monetary systems flip the traditional governance model on its head. Instead of decisions being made by a select group of officials, these systems rely on distributed consensus mechanisms where participants collectively validate transactions and propose changes. Bitcoin's proof-of-work system allows miners worldwide to compete in validating transactions and securing the network. Any major protocol changes require broad agreement among miners, developers, and users, preventing unilateral shifts in monetary policy.

Decentralized Autonomous Organizations (DAOs) take this concept further by enabling token holders to vote on governance issues. Between 2020 and 2021, the value of assets held in DAO treasuries grew from $380 million to $16 billion, highlighting growing trust in community-driven financial management. However, participation remains a challenge: less than 10% of users actively vote, leaving decision-making concentrated among a small, engaged minority.

The SushiSwap community illustrates these tensions well. In March 2022, the community debated creating legal structures to address regulatory risks while staying true to their decentralized principles. One community member captured the underlying concern: "As long as the final legal structure doesn't force Sushi to move away from offering their services globally to all humans equally. We cannot afford to compromise our core crypto ethos in order to appease increasing global 'regulatory demands.'"

Financial Sovereignty

The governance structure of a financial system defines the level of financial autonomy available to individuals. Central banks represent the traditional model, where governments maintain control over currency and monetary policy, allowing them to address economic crises, manage inflation, and stabilize financial systems. Yet this centralized control often limits individual financial freedom: 1.4 billion adults worldwide currently lack access to a financial account.

Decentralized systems offer a different vision, empowering individuals and communities to manage finances independently of central authorities. For the unbanked population, DeFi provides an opportunity for inclusion and economic self-determination. However, private digital currencies like stablecoins could compete with government-issued money, potentially undermining central banks' ability to execute effective monetary policies. In the first quarter of 2025, corporations acquired over 196,000 BTC, well above the year's new supply of approximately 60,000 BTC, signaling a strategic pivot away from traditional systems. With 93% of central banks now exploring CBDCs, the future likely holds a coexistence of centralized and decentralized systems, each catering to different priorities.

Transparency and Accountability

Trust in financial systems thrives on openness and clear lines of responsibility. In recent years, central banks have embraced a more open approach. The Federal Reserve and the European Central Bank now share detailed reports, hold press conferences, and communicate policy decisions through various channels. The IMF revised its Code in April 2019, emphasizing governance, policies, operations, outcomes, and external relations to promote openness, noting that "transparency and sound policies are better seen as complements." However, central banks must still balance openness with protecting sensitive information. The Federal Reserve delays meeting minutes to avoid market disruptions, and stress test methodologies often remain confidential to maintain financial stability.

Decentralized systems take a different route, relying on open-source designs and public ledger technology. Bitcoin and Ethereum record every transaction on a blockchain, creating a permanent, tamper-proof audit trail accessible in real time. The underlying code, including Bitcoin's fixed supply of 21 million coins and its halving schedule, is publicly available for verification. Despite this transparency, pseudonymity poses challenges: while transaction details are public, linking wallet addresses to real-world identities is difficult.

On accountability, central banks operate under a framework of institutional oversight, with Federal Reserve Chair Jerome Powell regularly testifying before Congress. This structure ensures that when issues arise, there is a clear authority responsible for addressing them. In decentralized systems, accountability is distributed across networks, shared among participants, developers, and governance protocols. While this reduces reliance on a single entity, it can create accountability gaps. Without a central authority or customer support, resolving issues often falls to the community.

Comparing the two systems side by side: central banks offer limited public disclosure but government oversight and audits; decentralized systems offer full public ledger visibility with community governance and on-chain voting. For speed, central bank international transfers can take days; decentralized systems settle in minutes to hours. For cost, central banks charge high fees for cross-border transfers; decentralized systems offer low transaction fees. For access, central banks require a bank account and ID; decentralized systems require only internet access.

Efficiency, Speed, and Access

Traditional centralized systems rely on intermediaries that can slow down transactions, though future Central Bank Digital Currencies could drastically improve transaction speeds. For comparison, Visa processes up to 24,000 transactions per second.

Decentralized networks show a wide range of performance capabilities. Bitcoin handles about 7 transactions per second, while Solana reaches 65,000 tps. Ripple settles in 3 to 5 seconds. Avalanche processes 4,500 tps in under 2 seconds, and Cosmos manages 10,000 tps. Ethereum has significantly reduced transaction fees through Layer 2 solutions, making it increasingly competitive with traditional banking infrastructure.

Accessibility is where the gap is most stark. In the U.S., about 6% of adults were unbanked in 2021, with 79% of these individuals earning less than $25,000 annually. Traditional banking creates barriers like minimum balance requirements, credit checks, and extensive paperwork. Decentralized Finance offers a solution by creating an open financial system accessible through any smartphone. DeFi users grew from 91,000 in January 2020 to nearly 5 million by July 2022. Globally, while 1.7 billion people remain without access to traditional financial services, about 1.1 billion of them own a mobile phone, making blockchain-based digital wallets a viable path to financial inclusion.

CBDCs could play a transformative role on the centralized side by acting as a digital gateway for unbanked populations. However, DeFi systems still face issues with interoperability, unpredictable network fees, and the technical challenges of managing cryptocurrency wallets.

Regulation, Security, and Stability

Centralized systems, like central banks, operate under well-established regulatory structures with clear accountability. The Federal Reserve System was created by Congress with goals of maximizing employment, stabilizing prices, and ensuring moderate long-term interest rates.

DeFi operates in a more uncertain regulatory environment, particularly in the United States where rules are still evolving. DeFi's reliance on automated software protocols instead of intermediaries complicates enforcement. As one attorney specializing in capital markets law explains, traditional finance is marked by intermediary entities creating trust and "enabling regulators to address them as 'a throat to choke' for the purpose of regulatory inquiries or enforcement." Without clear intermediaries, regulating DeFi becomes fundamentally challenging. In October 2022, the European Union launched a study on "Embedded Supervision of Decentralised Finance," exploring how to integrate regulatory checkpoints directly into blockchain systems for automated compliance.

On security, central banks invest heavily in cybersecurity to protect against systemic threats. The financial sector faced attacks that tripled between 2015 and 2021. Decentralized systems rely on cryptography and risk distribution, but in 2024 nearly $1.5 billion was lost to fraud and security exploits in DeFi. Unlike traditional banks, DeFi users are responsible for their own security. Common threats include flash loan attacks, reentrancy attacks, and rug pulls. A 2021 study found that half the tokens listed on the Uniswap protocol were scams, contributing to losses of nearly $1.3 billion that year.

On stability, central banks act as lenders of last resort, providing reliable settlement mechanisms and crisis management tools. CBDCs represent their digital evolution: as the Harvard Business Review notes, "CBDCs are direct liabilities of the central bank, just as paper cash is," making them a safer form of digital money than commercial bank-issued alternatives. Decentralized systems rely on algorithmic mechanisms and collateralization for stability, but these methods often fall short of the robust settlement functions provided by central banks. By March 2022, DeFi attackers had stolen nearly €1 billion in known funds, illustrating the real cost of algorithmic stability during stress.

Key Strengths and Weaknesses Compared

Central banks hold centralized authority over currency issuance and monetary policy, allowing them to implement measures aimed at financial stability. However, this concentration of power often limits individual financial autonomy. Decentralized systems like Bitcoin grant users direct control over their funds without needing approval from intermediaries, making it difficult for any central authority to freeze or restrict funds. The trade-off is that decentralized systems struggle when a unified response is necessary during market instability.

On transparency, central banks have historically operated with limited public visibility, though many are now taking steps toward greater openness. The Central Bank of Chile, for example, introduced a new transparency policy in February 2023. In decentralized systems, transparency is often built into the design through public blockchains, though some DeFi platforms concentrate decision-making power among a few entities, obscuring true decentralization.

Adoption patterns further highlight these trade-offs. By mid-2024, China's Digital Yuan had approximately 180 million wallets in use, representing about 12.76% of the population. In contrast, less than 0.5% of Nigeria's population uses the eNaira, even though over 50% have embraced cryptocurrencies, suggesting many users prefer the autonomy of decentralized systems over government-managed digital currencies.

For those looking to better understand decentralized finance, Decentralized Masters offers educational resources to navigate these complexities. Hybrid models that combine the stability of centralized systems with the flexibility of decentralized ones may shape the future of monetary policy.

Future of Monetary Policy

Monetary policy is undergoing a transformation, blending the roles of central banks with decentralized systems. Stablecoin circulation has doubled in just the past 18 months, and projections suggest that the total value of issued stablecoins could hit $2 trillion by 2028. Central banks are exploring tokenized systems that leverage blockchain for greater efficiency. Hyun Song Shin from the BIS highlights this potential: "The next-generation monetary system with central bank reserves at the core promises to deliver far-reaching benefits." A joint report by the New York Federal Reserve and the BIS demonstrated how smart contracts could streamline monetary policy, enabling faster creation or adjustment of financial facilities.

The Stablecoin Revolution

Stablecoins are becoming a bridge between traditional finance and DeFi. While they currently account for less than 1% of daily money transfers, by early 2025 they were handling 3% of the $200 trillion in global cross-border payments. Major financial institutions are experimenting with tokenized deposits and stablecoin integration to enhance efficiency and explore new business opportunities. However, stablecoins still face hurdles around singleness, elasticity, and integrity that limit their ability to serve as the bedrock of the monetary system.

Why This Matters for Your Financial Future

Understanding these shifts is crucial for staying financially informed. Around 1.4 billion adults worldwide remain unbanked, and decentralized finance offers a lifeline, enabling access to financial services regardless of location, credit history, or economic status. However, navigating the DeFi space requires a clear understanding of its complexities. Issues like regulatory uncertainty, security vulnerabilities, and wealth concentration, where just 0.01% of Bitcoin wallets control over 58% of the supply, highlight that decentralization alone doesn't guarantee fairness.

As digital assets gain traction, regulatory frameworks are beginning to take shape. Countries like Singapore, Luxembourg, and EU member states are introducing comprehensive digital asset rules. By January 2024, 130 nations including the United States were exploring the launch of their own CBDCs. Central banks will play a key role by establishing regulatory guidelines, providing foundational assets and platforms, and fostering collaboration between public and private sectors. The result will be a monetary system that is more efficient, transparent, and accessible, combining institutional stability with cutting-edge technology.

This transformation is redefining what money means: how it moves, who controls it, and how you can protect your wealth in a digital-first world.