Decentralized Finance (DeFi) lending protocols let you lend or borrow cryptocurrency without banks or intermediaries. These platforms use blockchain and smart contracts to automate the process, offering transparency and faster transactions. Lenders deposit crypto into liquidity pools and earn interest, while borrowers provide collateral (often over-collateralized) to secure loans. Smart contracts automate loan terms, repayments, and liquidations based on real-time market conditions, with interest rates driven dynamically by supply and demand.

DeFi lending is accessible to anyone with an internet connection, removing barriers like credit checks. However, risks include market volatility, smart contract vulnerabilities, and regulatory uncertainties. Platforms like Aave, Compound, and MakerDAO are popular choices, managing billions in assets. Staying informed, diversifying, and choosing audited platforms are essential steps to mitigate risks.

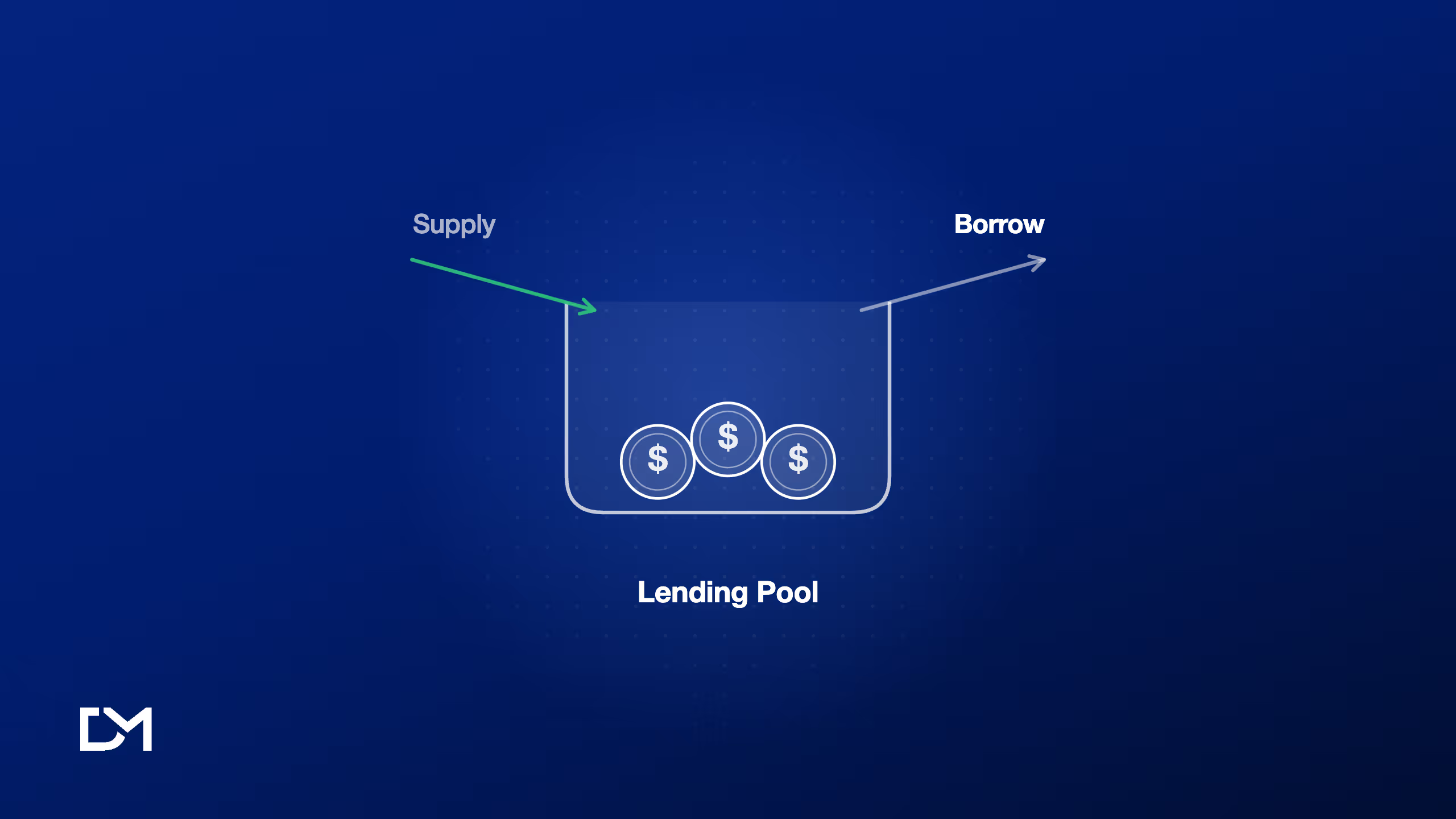

Main Components of DeFi Lending Protocols

Smart contracts are at the heart of DeFi lending protocols. These self-executing contracts have the terms of the agreement written directly into code and automate critical processes like issuing loans, managing collateral, and triggering liquidation when necessary. This automation eliminates the need for intermediaries, cutting down on paperwork and administrative fees.

Liquidity providers deposit crypto assets into shared lending pools, which borrowers can then access. By contributing to these pools, liquidity providers earn rewards from transaction fees. Many platforms also issue LP tokens to represent a share of the pool, with perks like governance voting rights or yield farming opportunities.

On the borrowing side, users must provide collateral to secure their loans. To account for the volatility of crypto assets, borrowers are typically required to over-collateralize, meaning the value of their collateral must exceed the loan amount. Every transaction is recorded on the blockchain, creating a transparent and permanent record of activity.

How DeFi Lending Works: Step-by-Step Process

The lending journey starts with picking a reliable platform, connecting a cryptocurrency wallet, transferring assets to the platform's liquidity pool, and approving the transaction via the wallet. On Aave, lenders not only earn interest (APY) but can also use their deposited crypto as collateral for their own borrowing needs.

Borrowers begin by depositing cryptocurrency as collateral. The platform assesses the collateral value to determine the loan-to-value (LTV) ratio. A smart contract automates the loan terms, including interest rates and repayment schedules. Once approved, the loan is sent directly to the borrower's wallet. DeFi platforms process loans quickly, often within minutes, and monitor collateral-to-loan ratios in real-time. If the ratio dips below the required threshold, automated liquidation protocols kick in.

Interest rates in DeFi are shaped by factors like supply, demand, risk, and liquidity. Aave uses a utilization-based, kinked interest rate model that adjusts rates dynamically. Borrowers repay loans through smart contracts, which then release the collateral back to them. If the borrower defaults, the smart contract automatically triggers liquidation to recover the debt.

Collateralized vs Non-Collateralized Loans

Collateralized loans are the backbone of most DeFi platforms. Borrowers must deposit cryptocurrency assets as security, often requiring overcollateralization typically ranging from 150% to 300%. This structure reduces risk for lenders, as it replaces traditional credit checks with asset-backed guarantees. Collateralized loans are suited for long-term borrowing such as margin trading and liquidity provision, with liquidation risk applying if collateral value falls below required thresholds.

Non-collateralized loans provide unsecured access to funds. The primary example is flash loans, which require repayment within the same transaction. These are designed for advanced strategies such as arbitrage or portfolio rebalancing, and are more accessible since no assets need to be locked up. However, they carry higher risk for lenders since there is no asset protection, and they cannot function as long-term borrowing instruments.

Risks and Considerations in DeFi Lending

DeFi lending carries notable risks. Unlike traditional banking systems, there's no FDIC insurance or centralized safety net to protect funds. In 2020, DeFi protocols accounted for half of all crypto-related attacks, representing 20% of the total stolen volume. Vulnerabilities in smart contracts have led to losses totaling $9.04 billion across DeFi platforms to date.

Smart contracts are the backbone of DeFi lending but are not foolproof. Coding flaws can leave them open to exploitation. In January 2022, the Tinyman exchange suffered a breach resulting in over $3 million in losses. Reentrancy attacks like the infamous DAO hack of June 2016 drained $60 million worth of ETH. Choosing platforms that undergo rigorous audits and have strong community oversight reduces this exposure significantly.

Price swings can quickly reduce the value of collateral, triggering liquidations if it falls below the platform's required ratio. To protect against this, maintaining collateral ratios well above the minimum threshold and spreading collateral across multiple cryptocurrencies helps buffer against sudden market moves.

The regulatory environment for DeFi remains uncertain. Changes in regulations could impact how protocols operate, affect token values, or limit access to funds. Protocol-specific risks such as governance failures or rug pulls also pose threats. Staying updated on regulatory developments and researching the governance model of any protocol before committing funds is essential due diligence.

Conclusion

DeFi lending protocols have reshaped borrowing and lending by cutting out traditional intermediaries. By 2023, DeFi lending managed over $32 billion in total value locked, and by 2025 global users exceeded 7.8 million. DeFi lending offers improved accessibility, lower fees, and transactions often completed in under five minutes. Since 2021, however, over $6.7 billion has been lost to hacks and smart contract exploits. Platforms with audited protocols saw 94% fewer hacks by 2025, underlining the importance of security-focused protocol selection.

For those looking to deepen their understanding of DeFi, Decentralized Masters provides educational programs and mentorship opportunities for navigating decentralized finance confidently.