Decentralized finance is removing intermediaries from financial systems and replacing them with open, programmable protocols. Anyone with an internet connection can access the same financial tools that were previously gated by credit checks, geography, and institutional approval. The market was valued at $21.3 billion in 2023 and is projected to reach $616.1 billion by 2033, growing at roughly 40% per year.

This isn't hype. Total value locked in DeFi protocols hit $129 billion by January 2025. Institutional investors, including major banks and asset managers, are actively allocating to the space. The infrastructure is maturing, costs are falling, and the case for DeFi as a permanent part of the global financial system is getting stronger every year.

Four forces driving DeFi forward

More than two billion people globally remain unbanked, often due to economic instability or geographic barriers. DeFi eliminates these barriers entirely. There's no credit check, no minimum balance, no branch to visit. Kotani Pay, supported by the UNICEF Innovation Fund, allows Kenyans to convert cryptocurrency into local currency using basic mobile technology. Leaf Wallet enables underserved communities and refugees to access digital financial services without standard banking requirements.

Traditional banks operate behind closed doors. DeFi uses blockchain to make every transaction transparent and immutable. Smart contracts on Ethereum automatically log timestamps, wallet addresses, and transaction details that cannot be altered after the fact. GreenCoffee tokenizes the value of coffee beans, allowing Ethiopian farmers, lenders, and processors to track payments in real time with automatic release on delivery confirmation.

DeFi also gives users full control over their financial assets. Unlike banks, which act as custodians and can freeze accounts, block transfers, or reverse transactions, DeFi users manage their own private keys and move funds on their own terms. Transactions don't require personal data, they run 24/7, and fees are typically 0.1 to 0.5% on decentralized exchanges compared to the higher costs embedded in traditional banking infrastructure.

Technology is rapidly closing the gap on DeFi's main historical weaknesses: cost and speed. Layer 2 solutions have reduced Ethereum gas fees by up to 90% and now account for over 45% of all DeFi transactions, with TVL on Layer 2 networks surpassing $42 billion by early 2025. Cross-chain bridging protocols hold $23.5 billion in TVL, enabling seamless movement of assets across blockchains. Tokenized real-world assets already exceed $250 billion, with Ethereum hosting roughly 55% of them.

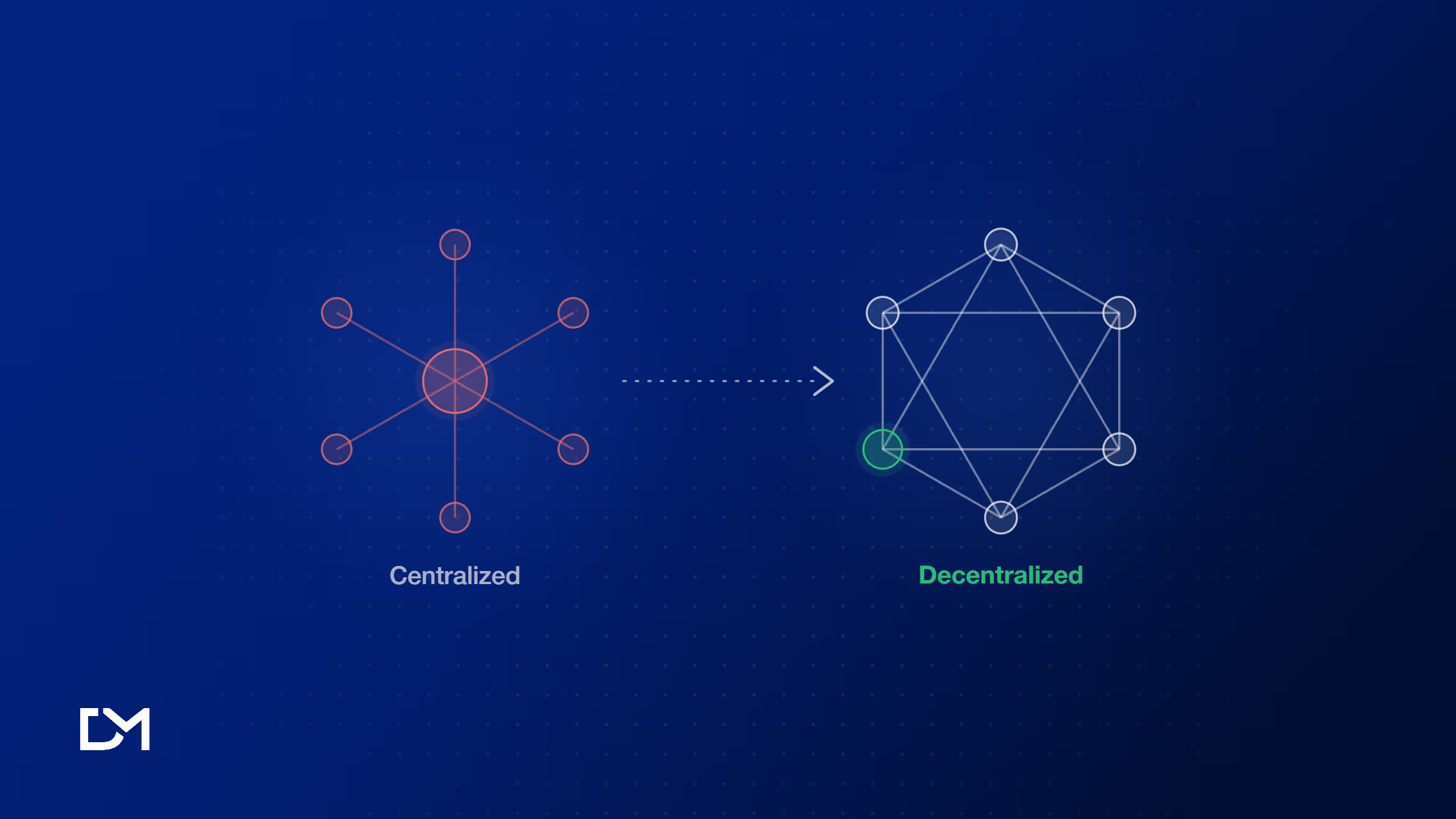

DeFi vs traditional finance

The core difference is custody and control. In traditional finance, banks manage your money, set the operating hours, determine who qualifies for services, and charge for every step of the process. DeFi puts users in direct control, operates continuously, requires no approval to access, and automates processes through smart contracts rather than staff and branches.

Traditional finance does hold certain advantages: FDIC insurance, established customer support, regulatory protections, and familiar user experience. These gaps are real, and DeFi is actively working to close them through insurance protocols, better interfaces, and clearer regulatory frameworks. But on the dimensions of transparency, cost, accessibility, and innovation speed, DeFi is already ahead and pulling further away. In 2021, total value locked in DeFi passed $80 billion. By January 2025 it had reached $129 billion, a 137% year-over-year increase.

Investment options for conservative investors

Overcollateralized lending

DeFi's growth has created a range of strategies that balance yield against risk. Overcollateralized lending through platforms like Aave, Compound, and Spark offers stablecoin yields typically between 2 and 4% APY. Aave, the largest lending protocol with $17.3 billion in TVL, delivers an average of 3.53% APY, with its USDT pool on Ethereum yielding approximately 4.5%.

Tokenized real-world assets

Platforms including Ondo Finance, OpenEden, and Maple Finance tokenize U.S. Treasury bills with yields between 4.8% and 5.1% APY. Institutional data shows that diversified DeFi portfolios allocating across liquid staking, overcollateralized lending, automated market makers, and real-world asset yields have outperformed traditional fixed-income investments by 387 basis points.

Security and risk management

Security tools have matured alongside yields. Multi-signature wallets, hardware security modules, and DeFi insurance from providers like Nexus Mutual and Sherlock protect against smart contract exploits. Institutional-grade wallets now represent approximately 41% of DeFi TVL, up from 17% a year ago, confirming that sophisticated capital is increasingly comfortable with the space.

Where DeFi is headed

DeFi currently represents only 1% of global financial assets. The path to mainstream adoption runs through better user experience, clearer regulatory frameworks, and continued institutional infrastructure development, all of which are actively in progress. By 2025, institutional investors plan to increase digital asset allocations by 83%, DeFi trading volumes are projected to surpass $523 billion, and 57% of institutional investors have expressed interest in tokenized assets.

Derivative trade volumes hit a record $6.18 trillion in March 2025. The integration of DeFi into the global financial system is not a distant possibility. It is already happening, and the rate of adoption is accelerating.

Decentralized Masters provides the education and research frameworks to navigate this shift confidently. The platform's Gems Uncovered service and DeFi Accelerator program are designed to help investors participate systematically rather than speculatively.